I haven’t posted in a loooong time, and I have not traded

any energy stocks since then. I’m still

holding a bit of Whiting Petroleum (tragically). And have not bought back into any of the

other names I had owned at the start of last summer: Chevron, Chesapeake,

Apache, Freeport Moran, and later briefly EOG.

My sense is that we are not nearing the end of the troubles for oil companies. These are my thoughts on US focused E&P companies a the moment:

1) Efficiency

gains by drillers have been impressive

I would say that it was fairly obvious that the breakeven oil price would decline significantly as prices started to decline. There was already a trajectory of improving economics even before the price declines, but the falling oil price caused costs to fall even more dramatically. Improved economics (at a given price) have come from several different causes. The most obvious is service cost declines. When the rig count drops from 1800 to 800 there is more equipment and more people chasing an ever smaller amount of work. The result is service cost deflation. Secondly, more speculative efforts, like proving up new acreage, drilling outside of core areas, or drilling wildcat exploratory wells has declined. The rigs that are working are drilling wells that the operator has plenty of confidence in. As those more marginal areas are abandoned, the average amount of oil produced per well increases. Finally, drilling was already improving prior to the start of price declines in 2014, as things like frac designs and better drilling accuracy were delivering ever improving results. This process has continued.

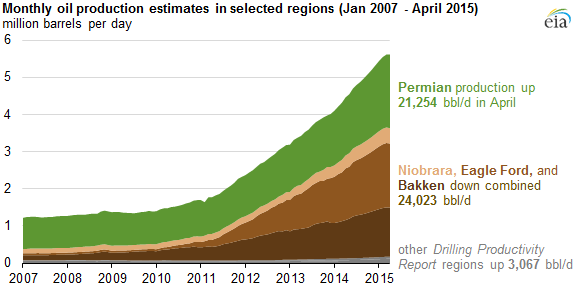

Permian, Bakken, and Eagleford new-oil production per rig

(from EIA drilling productivity report) are all up 40-50% yoy. Bakken and Eagleford production have peaked

for now because of the huge drop in rig count, but there is little doubt that

production would come back strong if oil prices were to stabilize even at

$70. When the crash started, many

analysts would talk about “break even” prices above that figure. Now breakeven for single well economics is

$40 or lower in the core areas of the big three oil regions.

Source: Baker Hughes

2)

Better break-even cost on new wells cannot necessarily save highly levered companies.

Their hedge books are

much weaker than a year ago. Many of

these companies have made more on their hedge books than on actually producing

oil as the price of oil has fallen. In

January of this year, most companies were somewhat protected because they had

hedged a portion of their production at very high prices. That will be much less true 6 months from

now.

Their debt service

costs are going to increase as they roll over debt. For small E&P companies, they will have

to issue new debt at much higher interest rates than they did a few years ago.

Price declines a year

ago were somewhat offset by increasing production, this will be not be the case

going forward. There was a big

backlog of uncompleted wells. For a

while they could cut capex but keep production strong by completing wells out

of their inventory. That will be less

true going forward, so many companies are seeing declines in cashflow from

lower prices, less hedged production, and now from lower volumes.

3) It is not clear that we need higher prices anytime soon to balance the market.

Many low

cost OPEC countries have a strong incentive to try to increase production as

prices decline. If your full cycle

cost is $10-15/bbl, and you need those oil dollars to fund your government, the

natural thing to do when oil drops from $100 to $50 is to try to produce more.

The US Rig count has declined from 1930 last september to

860 today. But the middle east rig count

has gone from a peak of 430 to 391 today.

There is hardly even a downward trend.

In fact, international rig counts (ex US and Canada) in general have

only declined from a 2014 average of 1330, to about 1200 today. These declines are very modest, and may not

even offset increases in production from Iraq and Iran, where production has

been artificially depressed by sanctions and instability. (Source Bakerhughes.com)

IEA reports in August that Non-Opec supply will still grow

1.1 million barrels per day this year, down from 2.4 million barrels per day

last year. They predict .2 mbd decline in

2016 for non-opec supply. OPEC supply

has increased by 1.4 mbd since November’s decision to protect market share and

not balance the market. Initially that

growth was driven by the Saudis but Iraq and Iran are likely to drive OPEC

supply in the future. Demand has grown

at a fairly constant pace, and has not accelerated noticeably since price

declined last year. In Q2 2015 there was

a record 3 mb/d of excess supply. This

is obviously not a sustainable situation.

|

| Source: IEA.org |

Conclusion: My instinct is to wait until we see some evidence that supply and demand are back in balance before buying oil stocks. There is a possibility that many US E&P companies will be able to survive if price can recover even to $60. But there is also a possibility that prices decline even further and we see a wave of bankruptcies. And so I will continue to wait.