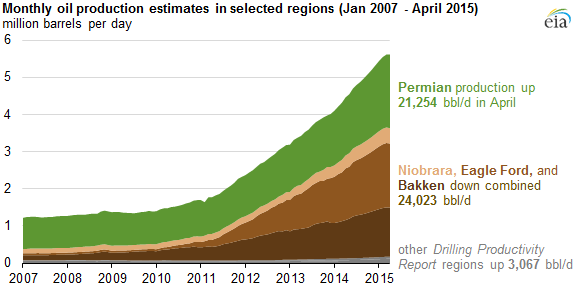

Of the three basins where the vast majority of recent production growth has been, two are now predicted by EIA to decline in April. There is a chance that we are seeing the peak in US production. Unfortunately, the market will still be far from balanced unless we get significant declines in production or increases in demand. Crude stocks have been building in the USA by just under 1 million barrels per day for the last 90 days. Now some of this is due to refinery turn-around season, perhaps 1/4 to 1/3 of the build if the past five year history is a model. We have had fairly high utilization rates during this turnaround season, which should have minimized the crude build under normal circumstances. Gasoline stocks are significantly above average as well.

Also, since we are a net importer why has our over production not simply displaced imports? The only answer that makes sense to me is that we have fully displaced all light crude imports and the refineries still are importing heavy crudes since that is what they are set up to refine. Almost all of the crude being produced from the tight oil plays is light crude. So the build in inventories is not just a sign of overproduction, it is a sign that there is a miss-match in the type of oil that is being produced and what the refineries want.

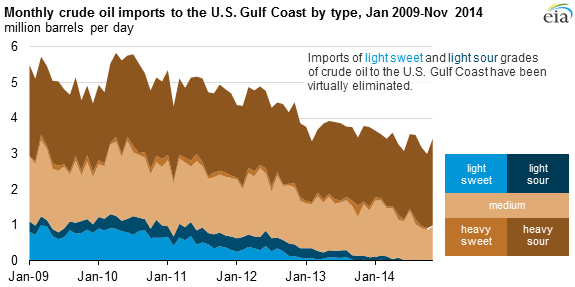

This EIA article from february shows how light crude imports have totally disappeared, and medium crude imports are on their way out too. I don't think there is available data showing how much inventory is which type of crude, but you can bet that the vast bulk of it is light crude.

So how do we get out of this situation of US inventory builds?

1) major increases in consumption- Hard to see this happening in as significant a way as it would need to to make a major impact. Even with very big consumption growth it couldn't really solve the glut of light oil, though it could make a dent in the global supply-demand balance.

2) US ends the oil export ban. This is an incredibly obvious thing to do, and just the type of bill the republican congress would love to pass. This is the easiest solution, but I would hate to be in the position of relying on the government to do something. If this happened we would be importing heavy oil and exporting light oil.

3) Refineries switch over to lighter grades- My non-expert sense is that this isn't something that happens fast. Also, only some switch-overs in the US Gulf Coast might create a glut of the heavy grades that come from Canada, Mexico, and Venezuela supporting the economics of those grades as well and disincentivizing massive change-overs to light grades. I don't think this solution is likely to be rapid enough to address the problem.

4) Exports of "lightly refined" crudes- This is what Valero and Pioneer did with lease condensate exports. They run it through a simple distilation tower and call it a refined product, which is thus eligible for exports. NGLs have always been exportable too. But why not go heavier and push the envelope further? I don't know enough about the rules to say whether this is really practical.

But if nothing happens, you could see even more egregious discounts for Eagleford and especially Bakken grades. Although spreads haven't apparently totally blown out yet, I would point out, that in percentage terms, the discounts are very high indeed. A $15 discount to Brent is more than 25% at current prices.